The Corporate File | Strategic Note

When the Honorable Prime Minister Narendra Modi compared today’s geopolitical environment to COVID-19, the signal was not about disruption.

It was about national preparedness and collective resilience.

In the gas sector, that signal is unmistakable:

The era of assuming stable energy flows is over.

The era of building resilient energy systems has begun.

🔶 The Real Shift: From “Fuel Source” to “Economic Backbone”

Gas is no longer a transition fuel in India’s growth narrative.

It is now embedded into the core of economic functioning:

• Household energy (PNG, CNG)

• Fertilizer production (food security)

• Power generation (grid balancing)

• Industrial fuel (cost competitiveness)

India’s push toward a gas-based economy is not environmental positioning alone.

👉 It is a macroeconomic stabilisation design.

Because:

• Gas pricing directly impacts inflation

• Supply disruptions immediately affect multiple sectors

🔶 War Changes Everything: From Supply Chains to Household Budgets

Global conflicts no longer remain geopolitical events.

They translate into economic shocks through energy systems.

In gas markets:

• LNG cargoes are diverted

• Shipping risks increase

• Spot prices become volatile

Macro Impact:

• Rising import bills

• Currency pressure

• Inflationary trends

Consumer Impact:

• Higher CNG and PNG prices

• Increased electricity tariffs

• Rising food prices (fertilizer linkage)

👉 War is no longer distant.

It is reflected in both balance sheets and household budgets.

🔶 The Structural Divide: Control vs Dependence

The gas ecosystem operates on a fundamental asymmetry:

Supply Controllers:

• Exploration & production companies

• LNG importers

• Pipeline and infrastructure owners

Gas Dependents:

• Fertilizer companies

• Power generators

• City gas distributors

• MSMEs and industrial clusters

👉 One side governs access and pricing

👉 The other absorbs volatility and margin compression

This is not a sectoral feature.

It is a governance reality.

🔶 PSU, Private, MSME: Unequal Resilience Across the System

PSUs:

• Policy-aligned

• Access to long-term contracts

• Infrastructure control

Private Players:

• Agile sourcing strategies

• Portfolio-based risk management

MSMEs:

• Highly price-sensitive

• Limited hedging ability

• Direct exposure to volatility

👉 MSMEs do not just consume gas.

They absorb systemic shocks.

A fragile MSME base is not a supply issue.

It is a macroeconomic vulnerability.

🔶 ESG Reality: Transition Fuel or Strategic Dependence?

Gas has been positioned as a cleaner alternative.

But governance questions are intensifying:

• Import dependence vs sustainability narrative

• Price volatility vs affordability

• Methane emissions vs transition benefits

👉 The ESG lens is shifting:

From “Is gas cleaner?”

To “Is gas controllable and resilient?”

🔶 Boardroom Reality: Governing Volatility, Not Just Operations

Gas businesses no longer operate in predictable environments.

They operate within a system influenced by:

• Geopolitics

• Policy intervention

• Currency fluctuations

• Infrastructure constraints

This demands a structural shift in governance:

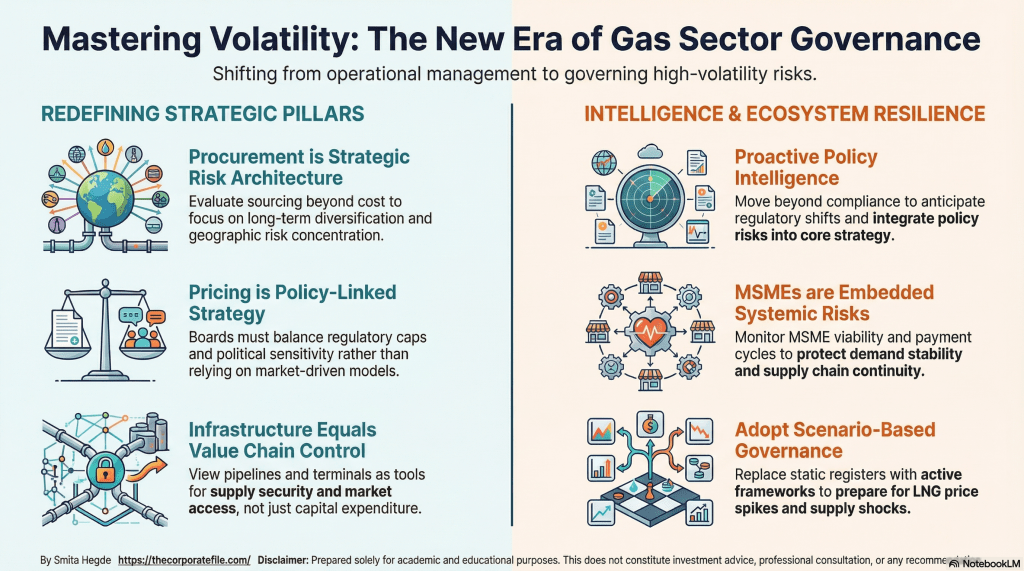

1. Procurement as Strategic Risk Architecture

Boards must evaluate sourcing beyond cost:

• Long-term contracts vs spot exposure

• Supplier diversification

• Geographic risk concentration

👉 Procurement is no longer transactional.

It is a risk management framework.

2. Pricing Governance Under Policy Constraints

Gas pricing is not fully market-driven.

Boards must navigate:

• Regulatory caps (CGD, fertilizers)

• Political sensitivity of price increases

• Demand elasticity

👉 Pricing is not just financial.

It is policy-linked decision-making.

3. Infrastructure as Control, Not Just Capacity

Pipelines, LNG terminals, and distribution networks define:

• Market access

• Supply security

• Competitive positioning

Boards must assess:

• Single-point failures

• Integration across value chain

• Strategic redundancy

👉 Infrastructure is not capex.

It is control over the value chain.

4. Policy Intelligence as a Core Governance Layer

The gas sector is deeply policy-driven:

• Allocation priorities

• Pricing frameworks

• Subsidy structures

Boards must move from reactive compliance to proactive alignment:

• Tracking regulatory shifts

• Anticipating policy direction

• Integrating policy risk into strategy

👉 Policy awareness is not advisory.

It is board-level intelligence.

5. MSME Ecosystem as a Governance Variable

Gas-dependent MSMEs influence:

• Demand stability

• Supply chain continuity

• Employment generation

Boards must evaluate:

• Supplier viability

• Payment cycles

• Cost pass-through capacity

👉 MSME stress is not external.

It is embedded systemic risk.

6. Scenario-Based Governance (War, Supply Shock, Currency)

Static risk registers are no longer sufficient.

Boards must build scenario frameworks for:

• LNG price spikes

• Supply disruptions

• Currency depreciation

👉 Governance must shift from reporting to preparedness.

🔶 The New Governance Metric

The gas sector will not be judged by:

• Volume growth

• Network expansion

It will be judged by:

• Supply security

• Pricing resilience

• Policy alignment

• Ecosystem stability

🔶 Closing Insight: Gas as an Economic Shock Transmitter

Gas connects multiple layers of the economy:

Energy → Industry → Food → Inflation → Policy

Any disruption flows through this entire chain.

When Narendra Modi emphasised preparedness,

the message was clear:

Resilience must be built into systems — not assumed.

In that reality:

Gas is not just an energy input.

It is a transmission mechanism of economic stability.

🔷 The Corporate File — Signature Metric

An economy is not stable because it has access to gas.

It is stable because it can secure, price, and govern gas without disruption.

Disclaimer: Prepared solely for academic and educational purposes. This does not constitute investment advice, professional consultation, or any recommendation

Connect on Linkedin www.linkedin.com/in/smita-hegde-90595b1b5

IndiaEnergy, CorporateStrategy, SupplyChainResilience, Geopolitics, GasEconomy, MSME, PublicPolicy, RiskManagement,

Leave a comment