Me (casually opening the SES Guidelines):

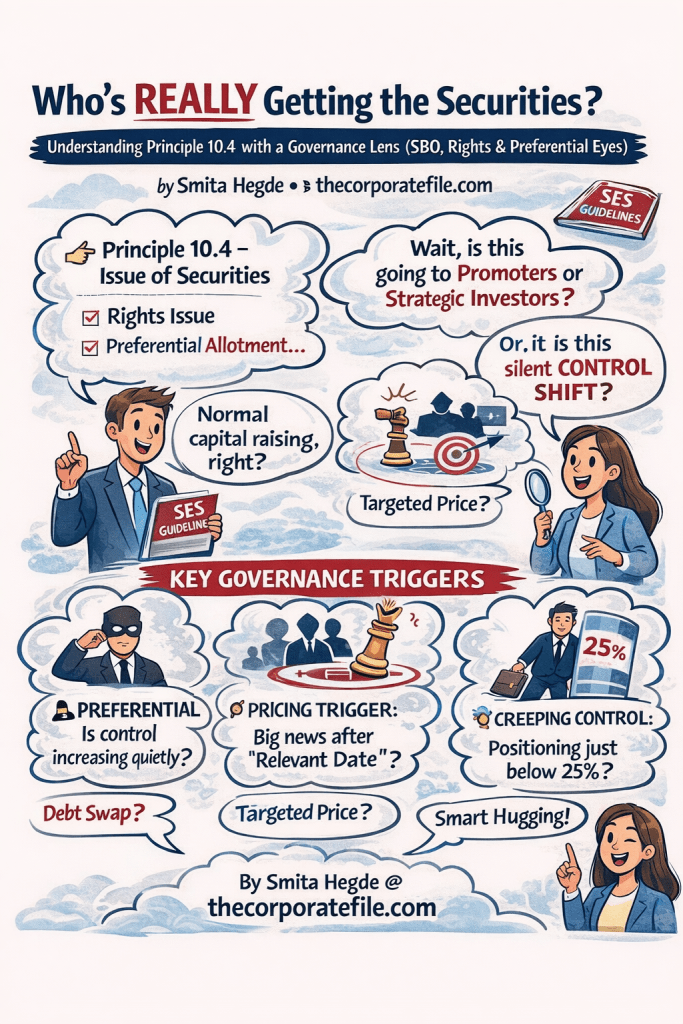

Alright… Principle 10.4 – Issue of Securities.

Rights issue, preferential allotment… standard capital raising.

source link

https://www.sesgovernance.com/assets/pdfs/proxy-advisory/1750172548_Proxy-Advisory-Guidelines_FY-2025-26_Website.pdf : Beyond Section 62: The Forensic Link Between SBO, SEBI SAST, and Security Issuancepage no.54

Me (reaching Question 7):

“Whether the issue is being made to promoters or strategic investors?”

…Okay. This is not routine.

This is where governance starts speaking.

The Conversation in My Head

Me 1 (compliance mode):

Check pricing ✔️

Check valuation report ✔️

Check approvals ✔️

Me 2 (governance mode):

Pause.

👉 Who is getting the shares?

Because that determines everything.

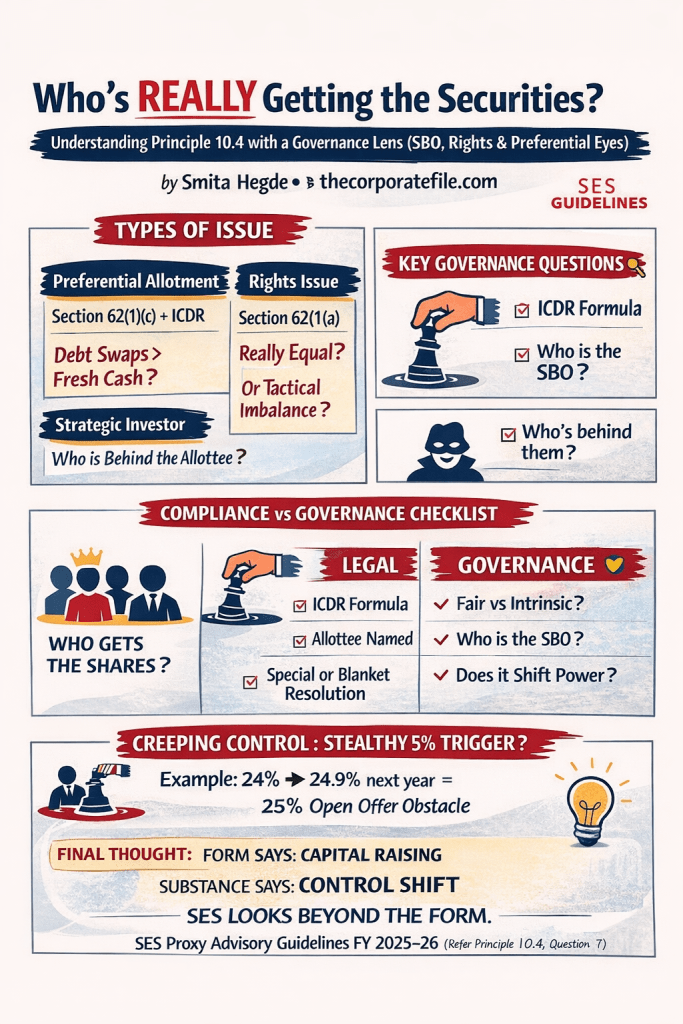

Layer 1: Preferential Allotment — The Silent Control Tool

Me:

Preferential issue is governed by:

- Section 62(1)(c) of the Companies Act, 2013

- Rule 13 of the Companies (Share Capital and Debentures) Rules, 2014

- Chapter V of the SEBI ICDR Regulations, 2018

Also me:

So yes — legally compliant.

But if allotted to promoters…

This could be:

- Increasing promoter stake quietly

- Structuring control below thresholds under SEBI SAST Regulations, 2011

- Diluting minority influence

👉 Not just capital raising — potential control engineering

🔍 Governance Lens 1: “Skin in the Game vs Free Ride”

- Fresh cash coming in? → genuine capital

- Debt conversion? → stake increase without liquidity

👉 If no real money enters → not growth, just control shift

🔍 Governance Lens 2: “Pricing Arbitrage”

- ICDR formula followed ✔️

- But timing manipulated ❓

👉 Good news after pricing = hidden discount to promoters

Layer 2: Rights Issue — Looks Fair, But Is It?

Me (relieved):

Rights issue = Section 62(1)(a) → offered to all shareholders.

Me (thinking deeper):

But what if:

- Promoters renounce strategically?

- Or subscribe disproportionately?

👉 End result:

- Promoter stake increases

- Minority diluted indirectly

🔍 Governance Lens 3: “Substance over Form”

- Form: Equal opportunity

- Substance: Control consolidation

Layer 3: Strategic Investors — The “Grey Zone”

Me:

Oh nice, a strategic investor is coming in.

Also me:

Wait… who exactly?

Because legally:

- Still falls under Section 62(1)(c) + ICDR

But governance-wise:

👉 Is this truly independent?

👉 Or a “friendly party”?

Enter the Real Game Changer: SBO (Significant Beneficial Ownership)

Me (now fully alert):

- Section 90 of the Companies Act, 2013

- SBO Rules, 2018

👉 Legal ownership ≠ Real ownership

🔍 Governance Lens 4: “Masked Allottee Risk”

Ask:

- Who is the ultimate beneficial owner (UBO)?

- Is there indirect promoter linkage?

👉 If unclear → assume control may be hidden

The Most Ignored Risk: Creeping Control

Me (connecting dots):

Under SEBI SAST Regulations, 2011:

- Promoters can increase up to 5% annually

But…

👉 24% → 24.9% = strategic positioning below 25% trigger

🔍 Governance Lens 5: “Creeping Control Calculator”

- Check post-issue voting power

- Not just % change

👉 Is this avoiding open offer intentionally?

The Hidden Red Flag: Blanket Resolutions

Me (frustrated):

“Approve issuance to any investor anytime”

👉 Legally valid

👉 Governance-wise dangerous

🔍 Governance Lens 6: “No Name, No Accountability”

If investor not identified:

👉 This is future dilution without transparency

Bringing It All Together — My Thought Flow

When I read this, I didn’t see a checklist.

I saw a forensic governance framework:

Step 1: Legal Structure

- Section 62 → issuance

- ICDR → pricing

- SAST → control

- SBO → ownership

Step 2: Governance Questions

- Who gets shares?

- Who gains control?

- Who is behind them?

The Real Governance Insight (This is the punchline 🔥)

Law checks compliance.

SES checks intention.

Summary Table (Compliance vs Governance)

| Feature | Legal Requirement | Governance Expectation |

| Pricing | ICDR Formula | Fair vs intrinsic value |

| Identity | Allottee name | SBO (real owner) |

| Method | Section 62 | Why not Rights Issue? |

| Control | SAST thresholds | De facto control shift |

When I Read This, I Thought Like This:

This one question connects:

- Section 62 → issuance

- ICDR → pricing

- SAST → control

- Section 90 → ownership

But SES…

👉 Asks one thing: Who really wins?

Source 📌

SES Proxy Advisory Guidelines FY 2025–26:

https://www.sesgovernance.com/assets/pdfs/proxy-advisory/1750172548_Proxy-Advisory-Guidelines_FY-2025-26_Website.pdf

(Refer: Principle 10.4 – Issue of Securities, Question 7)

Final Thought (Top Voice Mic Drop 🔥)

Form says: Capital Raising

Substance says: Control Transfer

And SES?

👉 SES reads substance.

Disclaimer: Prepared solely for academic and educational purposes. This does not constitute investment advice, professional consultation, or any recommendation

Connect on Linkedin www.linkedin.com/in/smita-hegde-90595b1b5

Leave a comment