The Corporate File | Strategic Note

When the Honorable Prime Minister Narendra Modi compared today’s geopolitical environment to COVID-19, the signal was not about disruption.

It was about national preparedness and collective resilience

Because in 2026, disruption is no longer episodic.

It is structural.

The question is no longer whether shocks will occur.

It is whether systems are designed to absorb them without breaking.

At the center of that system lies one underestimated lever:

Mobility infrastructure.

Aviation looks like a market.

It behaves like a system.

Public discourse reduces it to ticket prices, fleet size, and passenger growth.

For the Boardroom—and for the State—this lens is insufficient.

Aviation is not a market.

It is a National Mobility System—a policy-calibrated architecture designed to ensure economic continuity, regional integration, and sovereign positioning.

I. The Governance Reality: Aviation Is Not a “Free Market”

At the surface, airlines compete.

At the system level, outcomes are structurally engineered.

Global access is not demand-driven—it is negotiated through bilateral agreements.

Airports do not behave like competitive assets—they function as regulated monopolies.

Even pricing is not fully market-led—fuel taxation continues to shape cost structures.

Strategic Insight:

Aviation is a policy-shaped competitive system.

The Board’s role is not airline management.

It is regulatory alignment and system positioning.

II. India’s Post-COVID Reset: From Survival to System Continuity

Where global aviation anticipated prolonged collapse, India executed resilience engineering.

This was not a bailout cycle.

It was controlled reactivation.

- Capacity was released in phases to prevent destructive price competition

- Connectivity was preserved to maintain national mobility

👉 The objective was not survival of firms—

it was continuity of the system.

III. The Dual Lens: ESG Constraints and Ministry Objectives

Aviation today is governed by two parallel forces:

global sustainability constraints and national policy design.

1. ESG as an Operating Boundary

ESG in aviation has moved beyond disclosure.

It now defines operating feasibility.

- Fleet strategy is increasingly tied to fuel efficiency and SAF readiness

- Carbon exposure is becoming a direct cost variable

- Access to capital is progressively linked to sustainability alignment

👉 ESG is no longer reputational.

It is cost, capital, and continuity architecture.

2. The Ministry Lens: Stability Over Pure Market Efficiency

Under the Indian policy framework, aviation is not treated as a discretionary sector.

It is treated as critical infrastructure.

Through initiatives like the UDAN Scheme:

- Connectivity is expanded beyond profitable metro routes

- Capacity is moderated to prevent systemic instability

- Market cycles are actively managed to avoid erosion

👉 The system is not optimized for maximum competition.

It is optimized for national continuity and integration.

IV. The System Architecture: A Four-Layer Stack

Aviation operates as an interdependent vertical system:

1. OEM Layer — External Dependency

Aircraft supply is controlled by a global duopoly—

Airbus and Boeing.

👉 Capacity expansion is constrained by global manufacturing cycles—not domestic intent.

2. Operator Layer — System Equilibrium

- Full-Service Carriers → Network stability

- Low-Cost Carriers → Scale efficiency

👉 System health depends on equilibrium—not dominance.

3. Infrastructure Layer — The Binding Constraint

Airports define the upper limit of growth:

- Slot scarcity

- Runway capacity

- Airspace congestion

👉 This is the system’s hard ceiling.

4. Regulatory Layer — The Control Engine

Governed by the Directorate General of Civil Aviation and the Ministry:

- Safety systems

- Route economics

- Competitive balance

👉 This layer determines how the system behaves under stress.

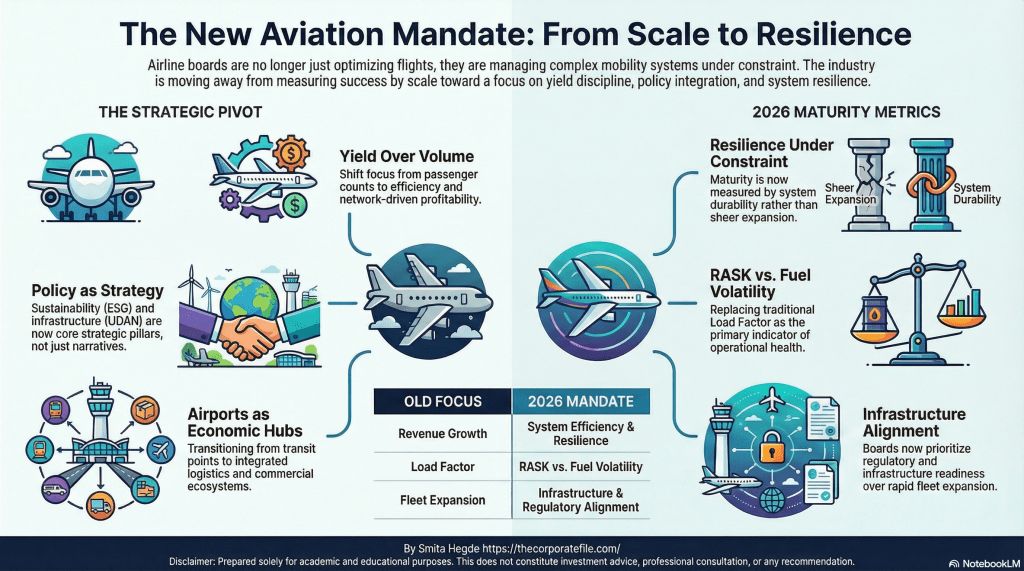

V. Boardroom Governance: The Mandate Has Shifted

Boards are no longer optimizing airlines.

They are managing mobility systems under constraint.

1. From Volume to Yield Discipline

The central question has changed:

❌ How many passengers?

✅ At what efficiency and yield?

- Network design now drives profitability

- Capacity discipline reduces volatility

👉 Growth without yield discipline leads to system dilution.

2. Policy Integration as Strategy

UDAN: Aviation as Infrastructure

Creates new demand ecosystems beyond metros.

ESG: Constraint, Not Narrative

- SAF adoption

- Carbon-linked costs

- Efficiency-driven operations

👉 Aviation strategy now sits at the intersection of policy and sustainability.

3. Airport-Led Economic Systems

Airports are no longer transit points.

They are becoming:

- Logistics hubs

- Cargo gateways

- Commercial ecosystems

👉 Aviation is embedding itself into the national value chain.

VI. The Signature Metric for 2026

Aviation maturity is no longer measured by scale.

It is measured by resilience under constraint.

Shift in Board-Level Metrics:

- Revenue Growth → System Efficiency + Network Resilience

- Load Factor → RASK vs Fuel Volatility

- Fleet Expansion → Infrastructure & Regulatory Alignment

Closing Insight: The System Has Already Evolved

India is not building airlines.

It is engineering a National Mobility System.

- Airlines → Visible layer

- Infrastructure → Capacity backbone

- Regulation → Control system

👉 Together, they define mobility sovereignty.

The Corporate File — Signature Metric

A nation is not aviation-ready because aircraft can fly.

It is aviation-ready when it can:

design, regulate, and sustain a mobility system under disruption.

Disclaimer: Prepared solely for academic and educational purposes. This does not constitute investment advice, professional consultation, or any recommendation

Connect on Linkedin www.linkedin.com/in/smita-hegde-90595b1b5

Leave a comment