The Corporate File | Strategic Note

When the Honorable Prime Minister Narendra Modi compared today’s geopolitical environment to COVID-19, the signal was not about disruption.

It was about national preparedness and collective resilience.

In energy, that signal is unmistakable:

India cannot rely on markets alone.

It must actively manage, diversify, and future-proof its energy system.

🔶 The Reality: Oil Is Not a Free Market

Globally, prices are influenced by coordinated supply actions of

OPEC and OPEC+.

But in India, the deeper reality is internal:

• Retail fuel prices act as a fiscal lever

• Government intervenes during inflation cycles

• PSU margins are calibrated to prevent consumer shocks

👉 Oil operates as a part-market, part-policy-controlled system

📂 Case in Point: The Russian Crude Strategy

The Russia–Ukraine War disrupted global oil flows.

Market expectation: supply shock.

India’s response: system-level recalibration.

• Increased imports of discounted Russian crude

• Diversified sourcing beyond traditional suppliers

• Stabilized domestic cost structures

👉 This was not opportunistic buying.

It was system management under stress.

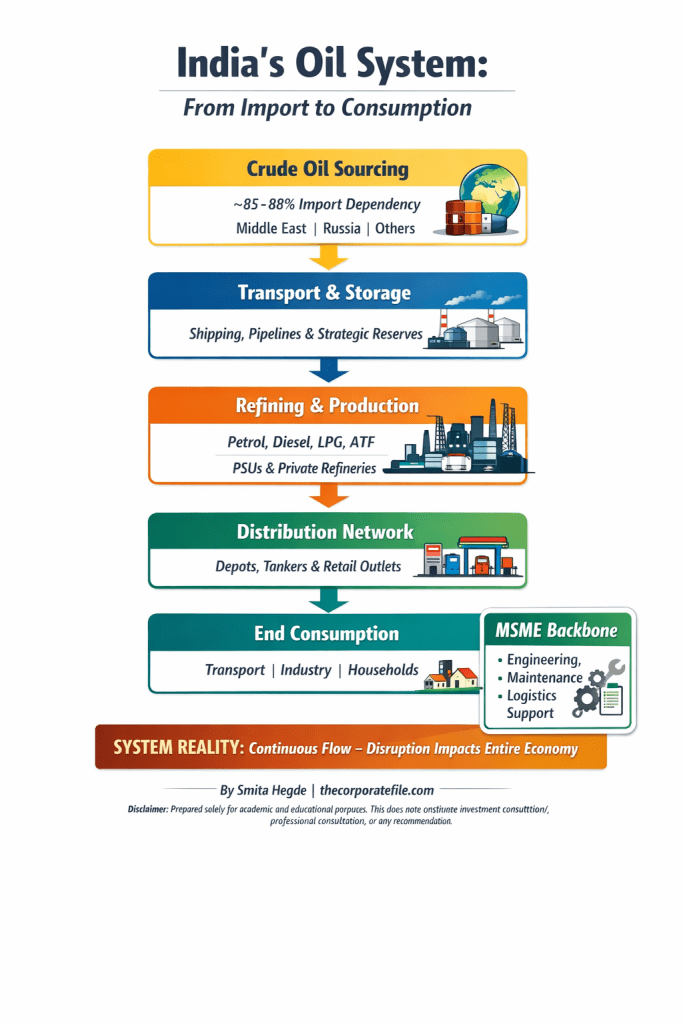

🔶 How the System Actually Runs

India’s oil system operates as a continuous, interdependent chain:

1. Import Layer (~85–88% dependency)

👉 https://ppac.gov.in/import-export

2. Refining Layer

• PSUs → stability

• Private → efficiency

3. Distribution Layer

• Nationwide logistics network

4. MSME Backbone

• Engineering, logistics, maintenance

👉 The system is integrated — not modular

🔶 Supply Chain Reality: Flow, Not Inventory

Oil is a flow system:

• Limited buffers

• Immediate disruption impact

🔶 PSU vs Private: A Designed Dual Structure

PSUs → Stability Layer

Private → Efficiency Layer

👉 Together, they ensure system resilience

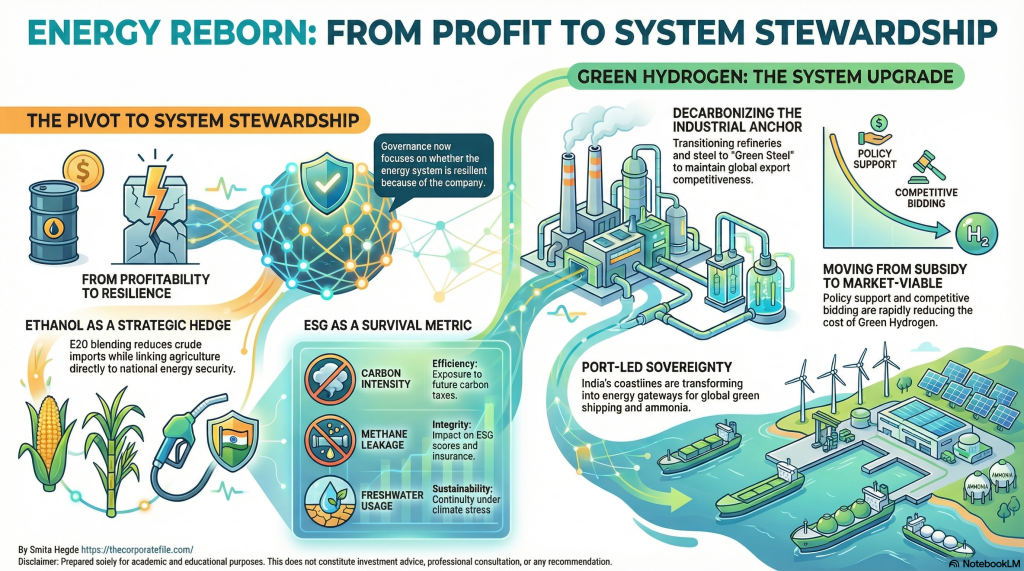

🔶 Governance Reframed: From Profit to System Stewardship

Oil companies are no longer just businesses.

They are system operators managing a national energy transition.

Boards now operate across three mandates:

• Commercial

• Policy

• Transition

Transition Mandate (Where Governance Is Redefined)

a) Ethanol: Reducing External Dependence

• E20 blending reduces crude imports

• Links agriculture to energy

• Acts as a currency hedge

b) ESG: From Narrative to Survival Metrics

| Environmental Factor | Focus Area | Why It Matters |

| Carbon Intensity | Efficiency | Exposure to future carbon taxes |

| Methane Leakage | Integrity | ESG score, compliance & insurance impact |

| Freshwater Usage | Sustainability | Operational continuity under climate stress |

👉 ESG is not reporting.

It is cost, risk, and continuity.

👉 The governance shift:

From

“Are we profitable?”

To

“Is the system resilient because of us?”

🔶 The Ultimate Hedge: Green Hydrogen (GH2)

If oil is a managed system, Green Hydrogen is the system upgrade.

It shifts India from an energy price-taker → price-maker.

1. The Industrial Anchor (Hard-to-Abate Sectors)

The focus has moved beyond pilots.

It is now about decarbonizing core industries:

• Refineries transitioning from grey to green hydrogen

• Steel sector adopting GH2 for “green steel” production

👉 This is not environmental positioning.

It is export competitiveness (CBAM readiness)

2. The Cost-of-Capital Revolution (SIGHT Program)

Under India’s Green Hydrogen mission:

• Large-scale production capacity has been awarded

• Costs are rapidly declining through competitive bidding

• Policy support (ISTS waivers) is reducing energy cost

👉 The shift:

Green Hydrogen is moving from subsidy-driven → market-viable

3. Port-Led Sovereignty: New Energy Corridors

India is building export-oriented green energy hubs:

• Western coast → Europe access

• Southern ports → green shipping

• Eastern hubs → fertilizer integration

👉 Coastlines are becoming future energy gateways

Closing Insight: Governance Has Already Shifted

Boards are no longer managing:

• Oil sourcing

• Refining margins

They are now managing:

👉 Electrolyzer → Hydrogen → Ammonia value chains

Green Hydrogen is not a future bet.

It is the next layer of energy sovereignty.

🔶 The New Metric: System + Transition Resilience

Energy companies must now be evaluated on:

• Supply continuity

• Import dependency reduction

• ESG readiness

• Transition execution capability

—not just financial performance

🔶 Closing Insight

India does not just consume energy.

It designs and manages an energy system.

Oil was the foundation.

Green Hydrogen is the upgrade.

🔷 The Corporate File — Signature Metric

A nation is not energy secure because it can buy energy.

It is secure because it can

control, transition, and sustain its energy system under disruption.

Disclaimer: Prepared solely for academic and educational purposes. This does not constitute investment advice, professional consultation, or any recommendation

Connect on Linkedin www.linkedin.com/in/smita-hegde-90595b1b5

Leave a comment