The boardroom was quiet.

Not the silence of agreement—

but of a decision already made.

A new Director was being proposed.

Highly capable. Strategically valuable.

But already serving on the board of a direct competitor.

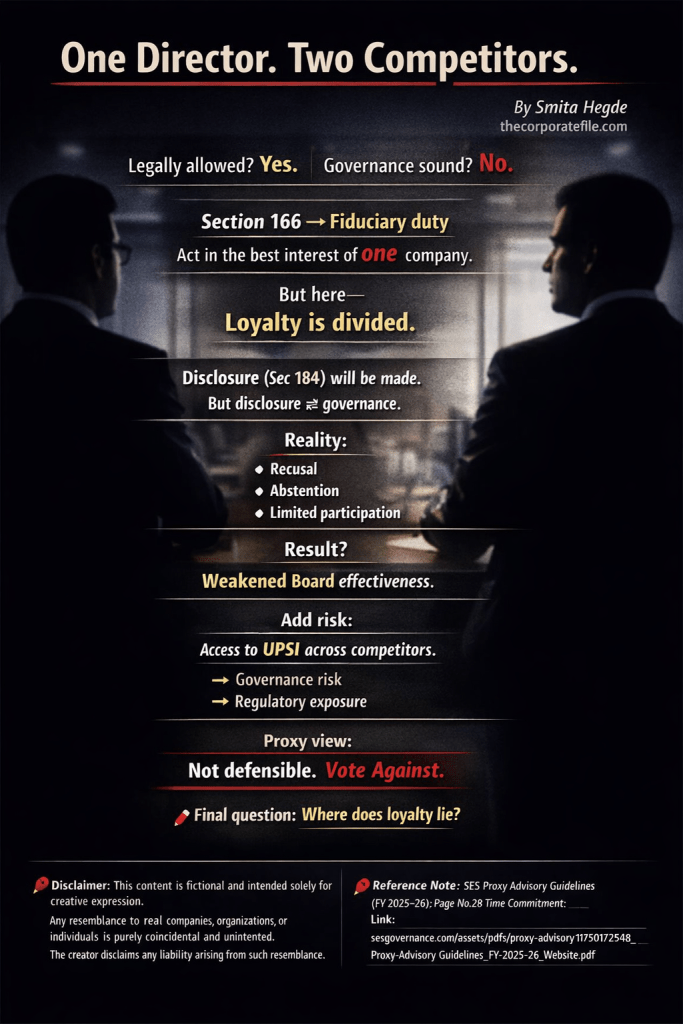

Under Section 166 of the Companies Act, 2013,

a Director must act in good faith

and in the best interests of the company.

So the question is direct:

Can one individual serve two competing companies at the same time—without compromising fiduciary duty?

This is not overlap.

This is fiduciary duality.

Yes, legally, the Board can appoint under Section 161.

But governance is not about what is allowed.

It is about what is defensible.

Under SEBI (LODR) Regulations, 2015:

- Regulation 4 requires integrity and avoidance of conflict

- Regulation 17 requires independent judgment

- Regulation 25 requires protection of stakeholder interests

A Director linked to a competitor is not merely interested.

He is structurally conflicted.

Disclosure under Section 184 will be made.

But disclosure is not governance.

Because the consequence is predictable:

- Recusal

- Abstention

- Limited participation

And a Director who cannot participate—

dilutes the Board, not strengthens it.

Now look at this from a proxy advisory lens.

Proxy advisors anchor their analysis in:

- Section 166 fiduciary duties

- SEBI LODR conflict framework

- SEBI Insider Trading Regulations on UPSI

A Director across competing boards is not just conflicted—

He is exposed to price-sensitive information across entities.

This is not just governance risk.

It is a regulatory risk zone.

Further, as per SES Proxy Advisory Guidelines FY 2025–26, Page 28 (Time Commitment):

Directors must have sufficient time to discharge their duties.

So this is not only a conflict issue—

It is also a capacity issue.

Proxy advisors therefore ask one question:

Is this defensible under fiduciary, governance, and market integrity standards?

And the answer here is clear:

Vote Against.

At this point, the Company Secretary becomes critical.

Under Section 205, the CS must:

- Advise the Board

- Ensure compliance

- Uphold governance standards

This is not procedural.

This is judgment.

The CS must flag the conflict,

assess the risk,

and ensure transparency to shareholders.

Because ultimately—

Shareholders decide under Section 152.

And their question is simple:

Where does loyalty lie?

The Board is not confused.

It is making a choice—

capability over integrity, framed as strategy.

And the truth is—

This is not a grey area.

It is a predictable governance failure.

And when trust breaks—

it does not erode.

It collapses.

Disclaimer: This content is fictional and intended solely for creative expression. Any resemblance to real companies, organizations, or individuals is purely coincidental and unintended. The creator disclaims any liability arising from such resemblance.

Connect on Linkedin www.linkedin.com/in/smita-hegde-90595b1b5

Leave a comment